BLOG / Employee Benefits

Managing RSU Withholding Tax: A Guide for Meta Employees

Restricted stock units (RSUs) have become a hallmark of the compensation packages of major tech firms like Meta, thanks to their effectiveness in linking employees’ financial interests with the company’s success. However, the tax implications of these equity-based incentives are more complex than those for regular cash salaries, often creating stress for individuals with RSUs as Tax Day approaches.

At Meta, it’s not uncommon for some employees to have more than half of their overall compensation in RSUs. Thus, for Meta employees with RSUs, it’s essential to understand how these units affect your tax situation to avoid potentially expensive mistakes.

Fortunately, by educating yourself and planning ahead, you can approach tax season with confidence, mitigate potential risks, and manage your equity compensation in a way that supports your broader financial goals.

RSUs at Meta

With the significant rise in Meta’s stock price in recent years, RSUs have become a valuable employee benefit. Depending on an employee’s role within the company, they may also provide a meaningful boost to overall compensation.

RSUs are grants of Meta stock (NASDAQ: META) that vest over a set period. Unlike stock options, RSUs don’t involve purchasing shares of Meta stock at a specific price. Instead, Meta promises to deliver a specific number of units once the employee meets certain conditions.

Meta RSUs vest over a four-year period, with 25% vesting each year on a quarterly basis. However, vesting schedules can vary, especially when it comes to new hire or promotional grants.

While this vesting schedule can be advantageous from a financial planning and cash flow perspective, it’s important to be aware of the associated tax implications.

RSU Taxation at Vesting

The IRS treats RSUs as supplemental income when they vest and therefore withholds taxes to offset federal and payroll obligations (Social Security and Medicare). Depending on where you live, you may also need to withhold taxes at the state level.

As of 2024, the IRS withholding rate is a flat 22% of supplemental income unless compensation exceeds $1 million. In this case, the withholding rate is 37%. However, your actual tax liability may be higher or lower depending on your taxable income for the year and other factors.

Meta employees also have the option to adjust their withholding rate for RSUs any time throughout the year. However, you must make the change at least one week prior to your quarterly vesting date for the new rate to apply. If you choose this option, careful planning is essential to minimize the amount you over- or underpay throughout the year.

Covering RSU Withholding Tax

When RSUs vest, they convert into Meta shares or the cash equivalent. This income, like a cash bonus, is subject to withholding taxes.

Yet, while withholding taxes from a cash bonus is relatively straightforward, RSUs introduce a layer of complexity. This is because the fair market value at the time of vesting depends on the current share price of Meta stock, which can fluctuate.

In general, there are three methods you can use to ensure you withhold taxes accordingly:

Sell to cover: As soon as your RSUs vest, Meta sells enough of the shares on your behalf to cover the tax obligation. You then receive the remaining shares. However, keep in mind that the IRS’s flat withholding rate of 22% typically doesn’t cover most Meta employees’ tax liability at the time of vesting. If you choose this option, you may owe additional taxes when you file your tax return.

Same-Day Sale: Meta immediately sells all RSUs as they vest and pays the tax obligation. You then receive the remaining cash.

Cash Payment: You cover the tax obligation by paying Meta the necessary amount in cash. In return, you receive all shares corresponding to your vested RSUs.

Most employers, including Meta, use the “sell to cover” strategy to handle taxes on their employees’ behalf unless an employee specifies otherwise. However, keep in mind if you receive Meta shares (and not cash) as your RSUs vest, you may also be subject to capital gains taxes.

RSU Tax Planning Considerations

The IRS mandates specific withholding rates from an employee’s supplemental wages, depending on their total compensation:

22% Withholding: This rate applies to supplemental wages up to $1 million.

37% Withholding: For supplemental wages exceeding $1 million, a higher rate applies.

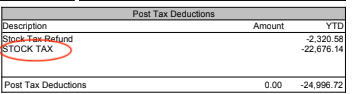

Some employees opt to withhold a higher amount from their supplemental wages to get closer to their actual tax liability. You can find your individual withholding amount on your paystub under “STOCK TAX.”

The above example is for illustrative purposes only.

If you find you ultimately owe more than you withheld throughout the year, you generally have three options:

Adjust your W-4 allowances. The Form W-4 is what you provide to your employer to dictate how much tax to withhold from your regular wages. By adjusting your allowances on this form, you can increase or decrease the amount you withhold from each paycheck. This method spreads out additional tax payments over the year, helping you avoid a large lump-sum payment during tax season.

Pay quarterly estimated taxes. Instead of adjusting W-4 withholdings, some Meta employees choose to make quarterly estimated tax payments directly to the IRS. While this method allows for more precise tax payments based on your estimated annual liability, it requires proactive financial planning and timely payments to avoid penalties.

Pay the difference when you file your tax return. If you owe additional taxes, you can simply pay the difference when you file your annual tax return. This method is straightforward and requires no changes to your current withholdings or estimated payments. However, if you owe too much, you could incur underpayment penalties from the IRS. These penalties can be expensive in some cases, especially with the IRS raising the annual interest rate for underpayments to 8%, as of 2024.

Be sure to consult with a financial planner like Simplicity Wealth Management or tax professional to ensure you’re making informed decisions and optimizing your tax approach.

Best Practices for Meta Employees with RSUs

For many Meta employees, RSUs represent a significant portion of total compensation, offering both financial rewards and potential tax implications. To ensure you’re making the most of your RSUs and aligning them with your broader financial goals, consider the following best practices:

Understand your tax situation. Knowing how RSUs impact your taxable income can help you anticipate potential tax liabilities and avoid surprises during tax season. It’s essential to review your RSU agreement and understand the vesting schedule. You can also monitor Meta’s stock performance to estimate your potential taxable income upon vesting.

Engage in proactive tax planning. Proactive tax planning can help you retain more of your RSU value by minimizing the associated tax liability. In addition, strategies like tax-loss harvesting or charitable giving can help offset your overall tax burden.

Plan for cash flow. Proper cash flow planning can help you meet immediate financial needs, invest for the future, and cover tax liabilities as they come due. You may want to consider selling a portion of vested RSUs to cover upcoming expenses or allocate the proceeds to tax-advantaged accounts, emergency funds, or other investment opportunities.

Seek professional advice. Given the complexities of RSU taxation and the potential financial impact, seeking advice from a professional with equity compensation expertise can be invaluable.

Making the Most of Your Meta RSUs

RSUs offer Meta employees a unique opportunity to share in Meta’s success. However, they also come with tax implications that can cause confusion and stress during tax season and impact your overall financial well-being. By understanding how your RSUs work, staying informed of your tax situation, and planning strategically, you can make the most of your RSUs while sidestepping potential pitfalls.

Remember: you don’t have to navigate the complexities of equity compensation on your own. Simplicity Wealth Management specializes in the unique financial planning needs of tech professionals with stock options and RSUs.

Our clients include current and former Meta employees managing the intricacies of their RSUs, providing us with the specialized knowledge to guide you through these complex decisions. Contact us to develop a personalized strategy to maximize your employee benefits and achieve your broader financial goals.

To discover more ways to maximize your equity compensation, download our free guide: The Insider’s Guide to Managing Stock Options & Restricted Stock.

Similar posts

How to Turn Your RSUs Into an Epic Vacation: A Step-By-Step Guide

Should You Use AI to Prepare Your Tax Return?

How the OBBBA Could Impact Your 2026 Tax Season